Policy Shocks & AI

解锁更多功能

登录后即可使用AI智能分析、深度投研报告等高级功能

关于我们:Ginlix AI 是由真实数据驱动的 AI 投资助手,将先进的人工智能与专业金融数据库相结合,提供可验证的、基于事实的答案。请使用下方的聊天框提出任何金融问题。

This report integrates four interlinked developments observed across 2024–2025 and into 2025–2026:

-

Business of detention: many jurisdictions have seen higher detention volumes and expansion of facilities operated by state or private contractors. Reports (Penal Reform International, Vera, etc.) document overcrowding, rising pre‑trial/immigration detention and increased role for for‑profit operators—even as human‑rights and litigation risks rise. Operational scale-up also drives procurement, facility services and security‑tech demand.

-

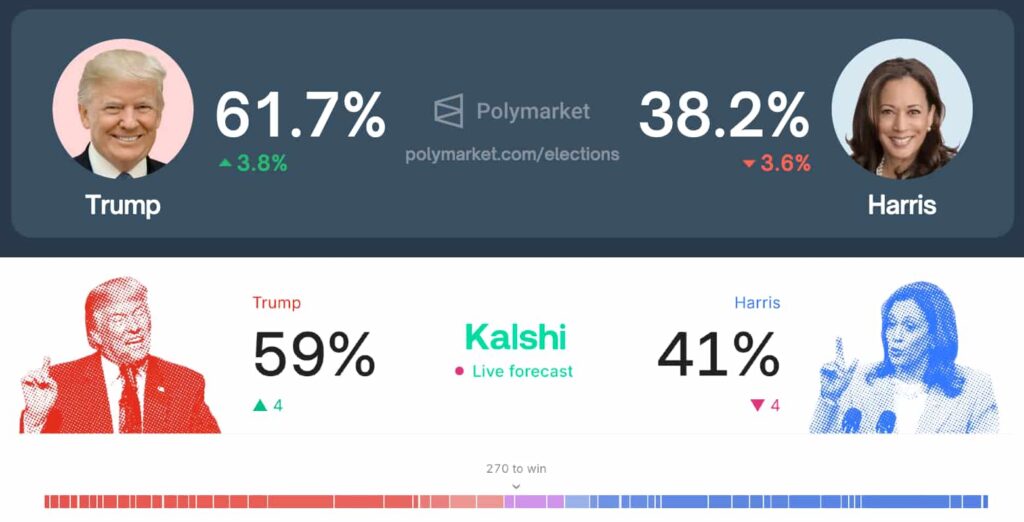

Prediction markets & elections: prediction market platforms (e.g., Polymarket, Kalshi, emerging exchanges) proved highly responsive during recent U.S. and global election cycles and are moving toward broader regulated footprints. Courts and regulators have shifted positions, enabling new products and institutional entrants; trading volumes and derivative innovation have accelerated. These markets now serve both information and financial liquidity roles in political risk pricing.

-

End of duty‑free / tariff changes: major economies have tightened low‑value/duty‑free thresholds and applied reciprocal tariffs in 2025, disrupting cross‑border e‑commerce flows and raising landed costs for low‑value goods. The policy mix includes suspension of de‑minimis treatments and broad reciprocal tariff packages that create supply‑chain friction and higher consumer prices.

-

AI in education: governments and sectors accelerated AI adoption in K‑12 and higher education (personalized tutoring, assessment, admin automation), while simultaneously developing governance (U.S. Dept. of Education guidance, national AI‑in‑education programs, and the EU AI Act). Countries pursue both capability building and risk controls (AI literacy, data governance, teacher training).

Causal and feedback links between these threads:

-

Political cycles and prediction markets: Election outcomes and campaign policy proposals (immigration enforcement, trade protection) are rapidly incorporated into prediction markets; market signals have in turn influenced investor and corporate expectations about tariffs and detention policy expansions.

-

Regulation and commercial scale: Regulatory openings for prediction markets and aggressive trade policy raise near‑term volatility. Firms in detention, security tech, legal services and cross‑border logistics face demand shocks tied to policy shifts (e.g., rapid expansion of detention capacity; relocation of supply chains due to tariffs).

-

Tariffs → EdTech costs and deployment: ending or reducing de‑minimis exemptions raises unit costs for low‑value EdTech devices (tablets, peripherals) and increases shipping complexity for schools and start‑ups that source hardware abroad—potentially slowing deployments or shifting procurement to local suppliers.

-

AI governance intersecting with detention and education: the EU AI Act and national AI guidance treat certain surveillance and assessment tools as high‑risk. AI systems used in detention (risk assessment, surveillance) or in education (automated exam proctoring, admissions/placement algorithms) face stricter obligations—raising compliance costs and liability exposure.

-

Information markets are maturing into policy‑sensitive instruments. Prediction markets now provide high‑frequency priors on elections and policy moves; institutionalization increases both accuracy and regulatory exposure.

-

Policy volatility (tariffs, immigration enforcement) is creating commercial growth in remediation services: compliance, logistics, substitute sourcing, legal and reputation management, and detention‑adjacent services—yet also attracting activist scrutiny and litigation risk.

-

AI adoption in education is no longer experimental: national strategies, professional development initiatives and platform rollouts are scaling in parallel with regulatory frameworks that treat some educational AI as ‘high‑risk’. This bifurcates vendors into (a) rapidly scaling but higher‑compliance products (assessment/proctoring, personalized learning) and (b) lower‑risk adjunct tools.

-

Supply‑chain and unit‑cost shocks from the end of duty‑free treatment will be most acute for low‑margin, high‑volume e‑commerce and for institutions buying low‑cost EdTech hardware. Procurement strategies and TCO models must be revisited.

-

Human‑rights and reputational risk is rising where surveillance AI and detention operations intersect. Increased detention capacity plus greater use of automated assessment/surveillance tools invites regulatory and NGO attention—particularly under EU rules and growing US scrutiny.

Risks

-

Regulatory & legal: stricter AI rules (EU AI Act), revived litigation on detention conditions, and evolving gambling/derivatives law for prediction markets can produce fines, injunctions and reputational harm.

-

Operational & supply chain: higher import costs, shipment delays and postal suspensions (after de‑minimis changes and tariff waves) threaten EdTech rollouts and consumer goods distribution.

-

Market & liquidity: prediction markets can amplify short‑term perceptions; regulatory reversals may cause rapid volume and price contraction for platforms and intermediaries.

-

Reputational / social license: firms providing services to detention systems or using surveillance‑grade AI risk NGO campaigns, investor divestment, and customer pushback.

Opportunities

-

Data & services: providers of high‑quality policy and event‑driven data (prediction market feeds, scenario modeling) can monetize demand from corporates, funds and policy teams.

-

Compliance & audit: advisory, compliance tooling, and AI‑safety products targeted at education and surveillance AI will see rising demand as regulators press for documentation, transparency and human‑in‑the‑loop safeguards.

-

Localized sourcing and hardware re‑engineering: companies that localize manufacturing or build higher‑value/low‑cost resilient supply chains can capture redistribution of procurement.

-

Responsible EdTech: vendors that design AI tools to meet ‘high‑risk’ compliance standards and embed AI literacy and explainability will gain public‑sector contracts and market trust.

For policymakers

-

Coordinate: align tariff, trade and technology policy with predictable timelines and clear exemptions for essential public‑sector procurements (e.g., education), minimizing disruptive cliffs.

-

Safeguard rights: explicitly limit and audit uses of surveillance AI in detention and border settings; require impact assessments and access to remedies.

For investors & corporates

-

Scenario plan: build top‑down scenarios incorporating election‑driven policy swings, tariff regimes and regulatory timelines for AI. Use prediction‑market signals as one input (not sole) to scenario weighting.

-

Reassess supply chains: quantify tariff and de‑minimis exposure for products (esp. EdTech hardware), evaluate nearshoring, and renegotiate vendor terms to include tariff pass‑through clauses.

For EdTech vendors & AI teams

-

Prioritize compliance‑by‑design: map AI features to EU/US/other compliance categories (transparency, human supervision, logging) and maintain technical documentation and quality management systems.

-

Differentiate product lines: offer a compliance‑assured tier for procurement by public bodies and a lighter commercial tier for lower‑risk use cases.

For NGOs & human‑rights advocates

- Monitor & audit: insist on transparency of AI systems used in detention, and demand independent impact assessments and grievance mechanisms.

Operational checklist (90‑day):

- Legal: inventory AI systems and identify any that fall under ‘high‑risk’ definitions; begin conformity assessments and documentation.

- Procurement: reprice hardware and cross‑border shipping line items with new tariff/de‑minimis assumptions; test alternative suppliers.

- Data & intelligence: subscribe to regulated prediction‑market feeds and policy trackers; incorporate into weekly scenario briefings.

- Reputation: prepare stakeholder communications addressing detention, AI use, and supply‑chain changes; pre‑empt activist narratives with transparency.

- Short term: run exposure analysis (tariff + de‑minimis) on top 50 SKUs and map AI systems to regulatory obligations.

- Medium term: pilot compliance upgrades (logging, human‑in‑loop) for any AI systems used in assessment/proctoring or surveillance.

- Long term: build partnerships across local manufacturing, compliance consultancies and data providers to turn policy volatility into competitive advantage.

数据基于历史,不代表未来趋势;仅供投资者参考,不构成投资建议

关于我们:Ginlix AI 是由真实数据驱动的 AI 投资助手,将先进的人工智能与专业金融数据库相结合,提供可验证的、基于事实的答案。请使用下方的聊天框提出任何金融问题。