Lithium Industry Capacity Expansion & Valuation Reassessment: Key Insights from Three Leading Miners

解锁更多功能

登录后即可使用AI智能分析、深度投研报告等高级功能

关于我们:Ginlix AI 是由真实数据驱动的 AI 投资助手,将先进的人工智能与专业金融数据库相结合,提供可验证的、基于事实的答案。请使用下方的聊天框提出任何金融问题。

相关个股

The article argues that lithium capacity in the new cycle has jumped 5-8x, but the market still uses old cycle price anchors, creating valuation re-assessment opportunities [1]. Three key miners exhibit distinct competitive advantages: 盛新锂能 (SZ002240) leads in capacity scale; 中矿资源 (SZ002738) boasts 100% resource self-sufficiency; 大中矿业 (SZ001203) shows the largest capacity elasticity [1]. Differences in resource self-sufficiency and capacity expansion paths will drive valuation divergence among individual stocks [1].

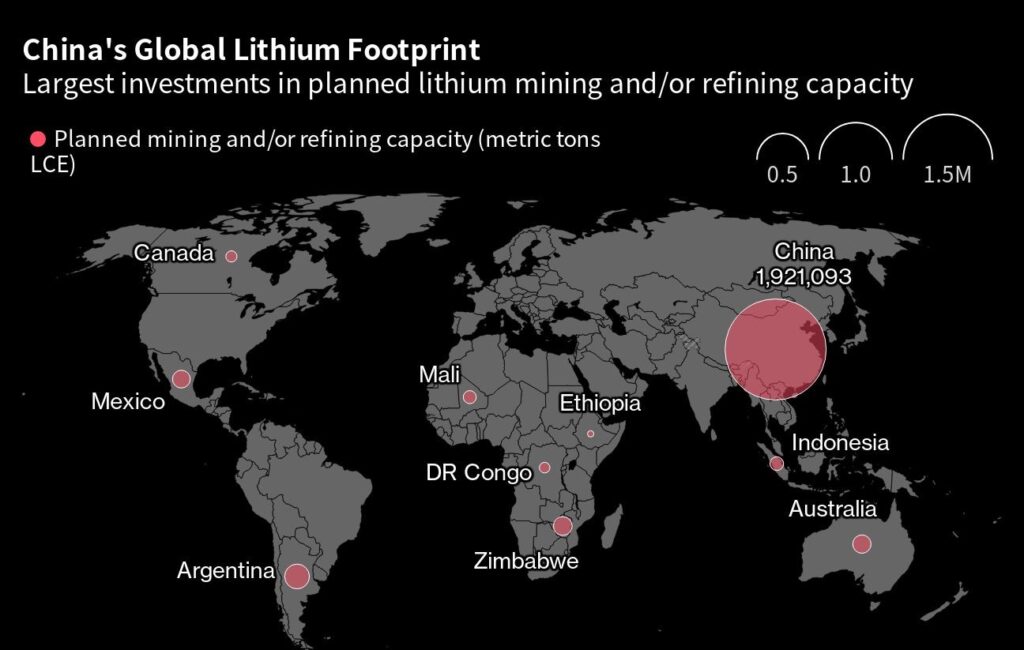

Global lithium carbonate capacity grew ~3x from 2022 to 2025 (57.61kt to 172.95kt) [2]. Africa’s lithium capacity surged ~29x (0.75kt to 21.9kt) [4], while Australia [5] and China’s salt lake lithium extraction [6] also saw significant expansion. The 2025 lithium industry enters a tight supply-demand balance with price recovery driving reversal [7], and storage demand emerging as a new growth engine [9]. 中矿资源 (SZ002738) has clear capacity data: 418kt/year lithium concentrate processing capacity and 6.6kt/year lithium salt capacity with high self-sufficiency [8].

Alignment: Both the original event and research confirm capacity expansion and valuation opportunities from outdated price anchors [1,2]. Contradictions: The original event claims a 5-8x jump vs global lithium carbonate capacity growth of ~3x (firm-specific vs global scope) [1,2]. Impact: Differentiated advantages will lead to stock divergence; storage demand sustains long-term growth [1,9].

Opportunities: Valuation re-assessment for strong fundamental miners [1,11]; storage demand-driven growth [9]. Risks: Capacity execution risks [5,6]; price volatility [7,10]; regulatory changes in key regions [4,5].

数据基于历史,不代表未来趋势;仅供投资者参考,不构成投资建议

关于我们:Ginlix AI 是由真实数据驱动的 AI 投资助手,将先进的人工智能与专业金融数据库相结合,提供可验证的、基于事实的答案。请使用下方的聊天框提出任何金融问题。